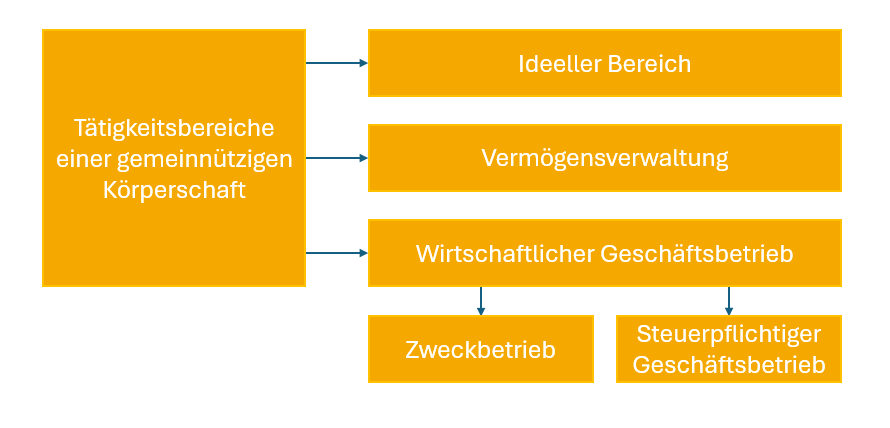

Tätigkeitsbereiche und steuerliche Behandlung

Die Tätigkeitsbereiche einer gemeinnützigen Körperschaft werden in den ideellen Bereich, die Vermögensverwaltung, den wirtschaftlichen Geschäftsbetrieb und den Zweckbetrieb unterteilt. Damit gehen auch Unterschiede in der steuerlichen Behandlung einher.

Ideeller Bereich

Im ideellen Bereich werden die satzungsmäßigen gemeinnützigen, mildtätigen oder kirchlichen Zwecke unentgeltlich verwirklicht. Die Einnahmen in diesem Bereich, wie beispielsweise Mitgliederbeiträge, Spenden, Schenkungen oder öffentliche Zuschüsse sind steuerfrei.

Vermögensverwaltung

Die vermögensverwaltende Tätigkeit besteht in der Nutzung von Vermögen, z.B. Zinsen aus Bankguthaben, Wertpapiererträgen oder Einnahmen aus Vermietung und Verpachtung. Diese Einnahmen unterliegen nicht der Körperschaft- und Gewerbesteuer. Die Steuerbefreiung von der Kapitalertragsteuer oder dem Zinsabschlag erfolgt nicht automatisch, sondern geschieht auf Antrag der gemeinnützigen Körperschaft.

Wirtschaftlicher Geschäftsbetrieb

Ein wirtschaftlicher Geschäftsbetrieb ist jede selbständige, nachhaltige Tätigkeit, durch die Einnahmen erzielt werden und die über den Rahmen der Vermögensverwaltung hinausgeht. Wirtschaftliche Geschäftsbetriebe, die die Voraussetzung eines Zweckbetriebes (siehe unten) nicht erfüllen, sind grundsätzlich steuerpflichtig, wenn die Bruttoeinnahmen (einschließlich Umsatzsteuer) im Jahr 35.000,- Euro übersteigen. Dabei handelt es sich nicht um einen Freibetrag, sondern um eine Freigrenze. Bleiben die Einnahmen unter dieser Grenze fällt keine Körperschaft- und Gewerbesteuer an, bei Überschreiten dieser Grenze unterliegt der Gewinn der Besteuerung. Die Gewinnermittlung ist erst vorzunehmen, wenn die Einnahmen einschließlich der Umsatzsteuer 35.000,- Euro übersteigen.

Zweckbetrieb

Der Zweckbetrieb ist eine Sonderform des wirtschaftlichen Geschäftsbetriebes, der steuerlich wie der ideelle Bereich behandelt wird. Um in den Genuss der damit verbundenen Steuervorteile zu kommen, muss der Zweckbetrieb dazu dienen, die steuerbegünstigten satzungsgemäßen Zwecke zu verwirklichen. Auch darf der Zweckbetrieb nicht mit anderen, nicht begünstigten gleichen oder ähnlichen Wirtschaftsbetrieben in größerem Umfang als nötig in Wettbewerb treten. Zweckbetriebe sind von der Körperschaft-, Gewerbe- und Vermögensteuer freigestellt. Bis zur Freigrenze von 17.500,- Euro besteht keine Umsatzsteuerpflicht Bei Überschreiten der Freigrenze gilt derermäßigte Umsatzsteuersatz von 7%.

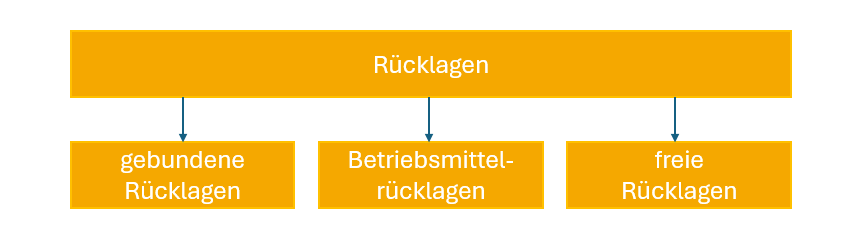

Rücklagen

Grundsätzlich sollen die erwirtschafteten Mittel eines Geschäftsjahres bis zum Ende des folgenden Jahres für steuerbegünstigte Zwecke verwendet werden. Die Bildung von Rücklagen dient dem Gebot der zeitnahen Mittelverwendung. Der Gesetzgeber lässt folgende Formen der Rücklagenbildung unter bestimmten Voraussetzungen zu:

- Gebundene Rücklagen

- Die Bildung der Rücklagen dient der Erfüllung der satzungsmäßigen Zwecke

- konkrete Zeitvorstellung (Zeitraum von 4-5 Jahren sollte nicht überschritten werden)

- Betriebsmittelrücklagen

- für periodisch wiederkehrende Ausgaben, wie z.B. Löhne, Gehälter, Miete

- in Höhe des Bedarfs und für eine angemessene Zeit

- Freie Rücklagen

- max. 1/3 des Überschusses der Einnahmen über die Ausgaben aus der Vermögensverwaltung

- 10% der Überschüsse aus Zweck betrieb, steuerpflichtigem wirtschaftlichen Geschäftsbetrieb bzw. Bruttoeinnahmen aus dem ideellen Bereich

Diese Rücklagen unterliegen nicht dem Gebot der zeitnahen Mittelverwendung und es gibt keine zeitliche Begrenzung. Sie sind jedoch auf Dauer zweckgebunden zu verwenden. Für den steuerpflichtigen wirtschaftlichen Geschäftsbetrieb dürfen sie nicht verwendet werden.

Cookie-Einstellungen

Cookie-Einstellungen