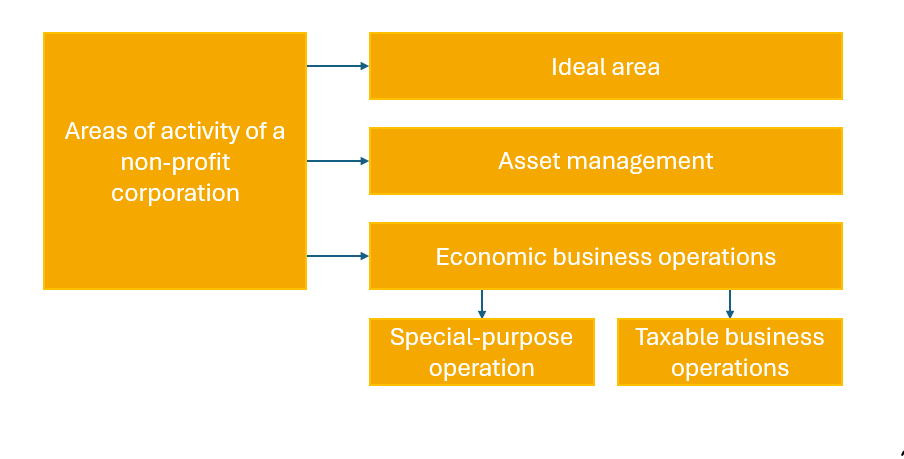

Areas of activity and tax treatment

The areas of activity of a non-profit corporation are divided into the non-material area, asset management, commercial business operations and special-purpose operations. This also results in differences in tax treatment.

Ideal area

In the non-material area, the statutory charitable, benevolent or ecclesiastical purposes are realized free of charge. Income in this area, such as membership fees, donations, gifts or public grants, is tax-free.

Asset management

The asset management activity consists of the use of assets, e.g. interest from bank balances, income from securities or income from letting and leasing. This income is not subject to corporation and trade tax. Tax exemption from capital gains tax or the interest deduction is not automatic, but is granted upon application by the non-profit corporation.

Economic business operations

An economic business operation is any independent, sustainable activity that generates income and goes beyond the scope of asset management. Business operations that do not meet the requirements of a special-purpose business (see below) are generally subject to tax if the gross income (including VAT) exceeds EUR 35,000 per year. This is not a tax-free amount, but an exemption limit. If the income remains below this limit, no corporation and trade tax is payable; if this limit is exceeded, the profit is subject to taxation. The profit must only be determined if the income including VAT exceeds EUR 35,000.

Special-purpose operation

The special-purpose business is a special form of commercial business that is treated in the same way as the non-material sector for tax purposes. In order to benefit from the associated tax advantages, the special-purpose enterprise must serve to realize the tax-privileged statutory purposes. The special-purpose business must also not compete with other, non-beneficial, identical or similar businesses to a greater extent than necessary. Special-purpose enterprises are exempt from corporation tax, trade tax and wealth tax. There is no sales tax liability up to the exemption limit of EUR 17,500. If the exemption limit is exceeded, the reduced sales tax rate of 7% applies.

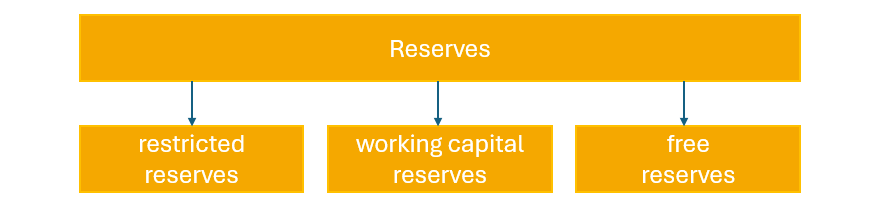

Reserves

In principle, the funds generated in a financial year should be used for tax-privileged purposes by the end of the following year. The formation of reserves serves to ensure that funds are used promptly. Legislation permits the following forms of reserve formation under certain conditions:

- Restricted reserves

- The formation of reserves serves to fulfill the statutory purposes

- Specific time frame (period of 4-5 years should not be exceeded)

- Working capital reserves

- for periodically recurring expenses, e.g. wages, salaries, rent

- in the amount required and for a reasonable period of time

- Free reserves

- max. 1/3 of the surplus of income over expenditure from asset management

- 10% of the surplus from special-purpose operations, taxable business operations or gross income from non-material activities

These reserves are not subject to the requirement to use funds promptly and there is no time limit. However, they must be used for a specific purpose in the long term. They may not be used for taxable business operations.

Cookie-Settings

Cookie-Settings